Table of Content

However, funds may not be drawn against a line after the draw period ends. Personal loans can also be used for a wide variety of purposes, and some lenders offer easy online applications with fast funding. However, you’ll need to have strong credit to get the best rates.

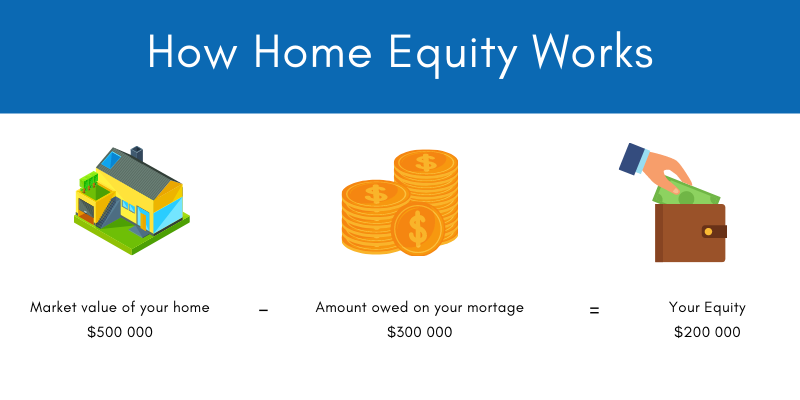

Is a type of loan that gives homeowners the chance to tap into the equity that they’ve built into their home. To clarify, home equity is simply the difference between the worth of your home and the remaining mortgage balance. The equity allows homeowners to have and use the collateral to borrow funds. For example, if you still owe $100,000 on your mortgage and your home is worth $250,000, you have $150,000 worth in equity. Both of these loans are types of mortgage loans that come with closing costs. Closing costs are the charges to pay your lender when you close on a loan.

The Bankrate promise

External third-party web sites will be presented in a new and separate content window. Clearview FCU does not provide, and is not responsible for, the product, service, overall website content, accessibility, security, or privacy policies on any external third-party sites. Many of these differences are some of the 10 Reasons Millennials Choose Credit Unions over banks. Before the Tax Cuts and Jobs Act, you could deduct only up to $100,000 of the debt on a home equity loan. The Balance uses only high-quality sources, including peer-reviewed studies, to support the facts within our articles. Read our editorial process to learn more about how we fact-check and keep our content accurate, reliable, and trustworthy.

Our editorial team does not receive direct compensation from our advertisers. At Bankrate we strive to help you make smarter financial decisions. While we adhere to stricteditorial integrity, this post may contain references to products from our partners. Suzanne De Vita is the mortgage editor for Bankrate, focusing on mortgage and real estate topics for homebuyers, homeowners, investors and renters. The offers that appear on this site are from companies that compensate us. This compensation may impact how and where products appear on this site, including, for example, the order in which they may appear within the listing categories.

Does a personal loan have lower interest rates than a credit card?

It will depend largely on the length and type of the loan (e.g., secured vs. unsecured) as well as the borrower’s credit history. A home equity loan is a type of secured loan in which the borrower’s home is used as collateral, whereas personal loans can be secured or unsecured by collateral. As personal loans tend to have a less intensive approval process than a home equity loan, they can generally be quicker and more straightforward to obtain. While home equity loans usually will take longer to be approved, they tend to offer a lower interest rate than a personal loan and potentially a higher loan amount as well. Before pursuing either option, however, it’s important to consider the amount you need and the intended purpose of your loan.

When your loan closes, you will own and be able to live in the home as you slowly repay the cost to purchase it. All the while, however, your lender retains some “rights” to the home, so to speak. That means that if you fail to make payments toward your loan, your lender may be able to take back your house and sell it to someone else to recoup their losses.

Home equity takes time to build

After you borrow a mortgage, that stake in the property becomes your equity, and it allows you to borrow more through a home equity loan. Cash-out refinance makes sense when current mortgage rates are lower than what you’re paying. You refinance your mortgage for a higher amount than you owe, and then “cash out” the rest to pay for the renovation. Home equity loans are a type of secured loan where your home acts as collateral. As mentioned in the chart, if you can't pay back your loan, the lender has the right to seize your home through the foreclosure process. The loan amount you qualify for is determined by factors including the amount of equity you have in your home, the value of the house, your credit history and ability to pay back the loan.

As listed in the above chart, personal loans are typically unsecured loans, meaning that you don't need to back up your loan with collateral like your car or your home. Lenders will also look at your credit score, income and debts when setting your interest rate and determining if you qualify for a personal loan. Focus your home equity financing on improving your long-term financial situation. Use it to add value to your home, consolidate and save money on your high-interest debt, pay for education , or pay for a significant emergency that your regular cash flow cannot cover. Many experts recommend against using home equity loans and HELOCs to fund vacations, car purchases, or high-risk investments.

Getting approved for a personal loan is usually faster than the approval process for a home equity loan. You can get cash in your account in as little as a business day, depending on the loan amount and the lender. Borrowers don't have to go through demanding processes like an appraisal and other reviews as they would for a home equity loan. Both types allow you to use funds for almost any reason, such as a home improvement project or debt consolidation, but it's important to know the differences between them. Your eligibility and personalized interest rate will be based on how well you meet a lender’s requirements. For instance, a higher credit score and lower DTI ratio should get you more favorable terms.

A reverse mortgage gives homeowners access to their equity without adding additional monthly payments to what may already be a tight budget. Choosing between a home equity loan and a HELOC depends on a borrower’s needs. For example, if you want a structured loan that will let you know exactly what your monthly payment will be and when your loan will be paid back, then a home equity loan is a great choice.

With this type of financing, you borrow a certain amount but repay only what you use. This may influence which products we review and write about , but it in no way affects our recommendations or advice, which are grounded in thousands of hours of research. Our partners cannot pay us to guarantee favorable reviews of their products or services. Considering taking out a home equity loan to consolidate your debt? Read on to learn the pros and cons of using a home equity loan for debt consolidation. If that’s the case, here are some other options you could consider.

Both home equity and personal loans offer advantages and large amounts of cash, depending on your requirements and financial situation. Either loan comes with risks and differing qualification requirements, too. Just as with home equity loans, you pay back your personal loan in regular monthly payments that include interest.

However, the confusion arises from the fact that it’s a mortgage taken out separately from – and often after – your primary mortgage. On a personal loan, the interest rate can be anywhere from 6% to 36%, depending on your credit history. For home equity loans, the interest rate can be as low as 1.89%, ranging upward to around 11.75% (depending on the loan’s length), with the average hovering around 4% to 5%. In a home equity loan, money is borrowed using the value of your home as collateral. So your maximum cash-back is equal to 80 percent of your home’s value minus your current loan balance.

Some online lenders say they can fund a loan the business day after you’re approved. The amount you get with a personal loan, on the other hand, is often based solely on your creditworthiness and finances. These loans are available in amounts up to $100,000, but you’ll need strong credit and low debt compared to your income to qualify for the largest loans. Personal loans are typically funded more quickly than home equity loans.

Let's take a look at the pros and cons of HELOCs and home equity loans. You can generally borrow around 80% to 85% of the value of your home, minus what you owe on your mortgage. Home equity loans may be taken out on a primary or secondary residence. Given the age requirement of a reverse mortgage, it is designed to be a resource for those who are near or in retirement.

No comments:

Post a Comment